The main mode of transportation for commercial purposes is now benefiting from the EV revolution. In the past 10 years, EV have gone from a niche segment to mass market. Medium- and heavy-duty trucks are following the same path.

The 3 core enablers

- Regulations. Most governments have major incentives to promote EV, such as

- tax breaks for vehicles, components, and infrastructures

- discounts on road tolls

- carbon tax

- and sales ban on internal-combustion-engine (ICE) vehicle

- Governments’ EV procurement

- Technology. To ensure large deployment, total cost of ownership (TCO) is important

- Industry players are accelerating innovations for key powertrain components, making EV trucks economically competitive with their diesel counterparts

- In the coming decade, we will continue to have major technological advances that continue to decrease costs for fuel cell systems, batteries and charging hardware

- Market dynamics and infrastructure.

- Climate change will incentivize fleet operators and OEMs to accelerate EV fleet adoption. But to reach scale, charging networks must expand. The rollout will require substantial investments, including ancillary products such as Battery Energy Storage Systems (BESS) to increase grid capacity.

Technologies for EV trucks

Electric powertrain is the go-to technology for EV trucks, mainly because of their advantages in emissions and cost.

Renewable diesel, renewable natural gas, and other eco-friendly fuels can help speed up the reduction of carbon emissions from existing diesel and natural gas vehicle fleets. Their benefit lies in their compatibility with existing infrastructure and engines, and they are already on the market, though in limited quantities. Production is anticipated to grow, driven by demand from sectors like aviation, shipping, and manufacturing. However, without policy incentives, these renewable fuels will continue to be more expensive than traditional fossil fuels and won’t be able to compete cost-wise with battery electric vehicle systems for most road transport uses over time.

Marching into a new world of business uncertainties

Beyond the choice of powertrains, many other future developments in the market for EV remain uncertain. We believe the following factors could be among the most important in shaping the industry’s future:

Technology development costs: Battery costs have already dropped over the past ten years and are expected to keep falling. More reductions are still needed to make these technologies economically viable.

Operational characteristics: EV trucks face operational challenges such as payload restrictions (due to battery weight), recharging times, and limited ranges.

Infrastructure availability: BEV trucks need new infrastructure to ensure widespread use. This includes a stronger electric grid and hydrogen refueling stations.

Beyond these factors, country-specific differences in energy prices and fleet-specific needs may lead operators to prefer one technology over another. For example, the cost of batteries goes up as the range they provide increases, so operators that mostly use trucks over short to medium distances or predictable routes may prefer BEVs. For long-haul use with less predictable routes, collaborating with a reliable charging infrastructure partner is necessary because of their shorter charging times and lower upfront costs. Overall, BEV trucks have an advantage in the EV market because they will be available at scale soon and will benefit from advances in technology.

Evolving supply and demand for EV trucks

Many fleet operators have announced decarbonization targets, and over 70 models of EV trucks are expected to be available by 2040 compared to 130 models available with diesel engines. Production volumes in China are high, maintaining a rate of 60,000 units per year, while Western counterparts produce less than half of this amount annually.

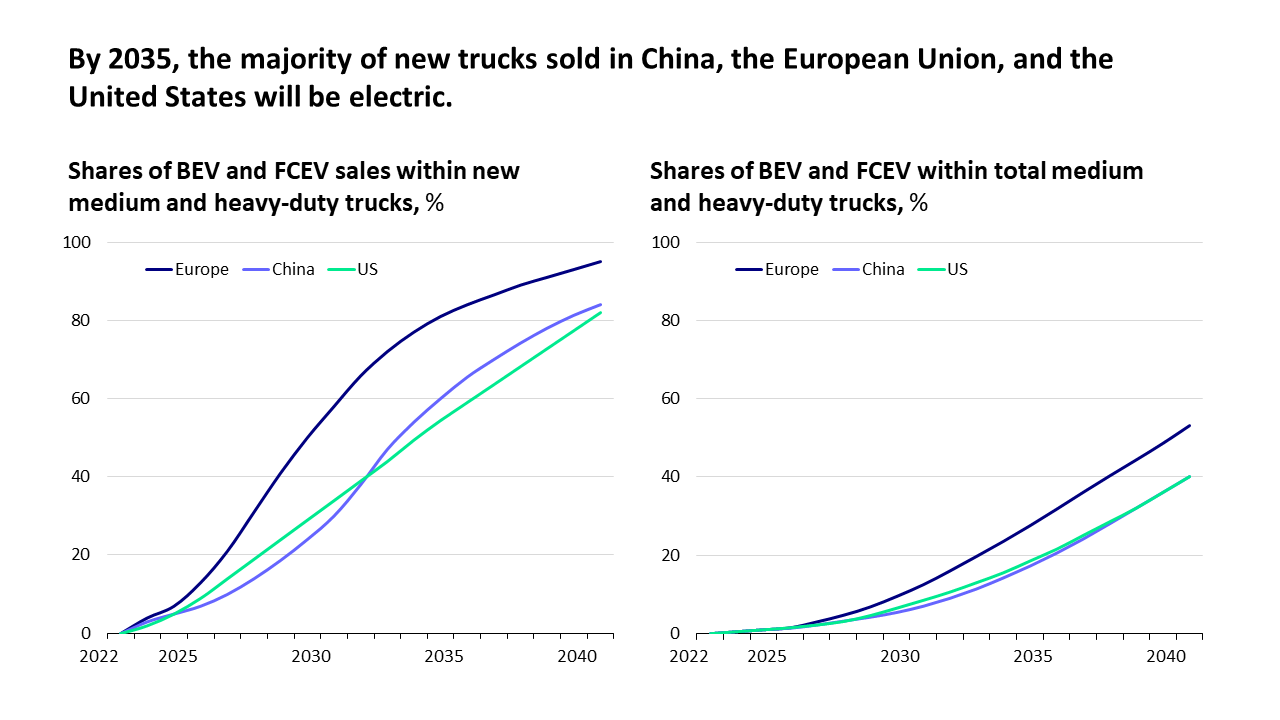

Demand for EV trucks is expected to increase significantly, partly because the total cost of ownership is expected to fall by about 10% over the next 5 to 10 years. By 2035, most new trucks sold in China, Europe and the United States will be electric.

By 2040, 85% of new trucks sold and 40% of all trucks on the road are expected to have a zero-emission powertrain. To meet future demand, the industry will need additional battery production capacity equal to 12 gigafactories by 2030. Moreover, EV trucks will add about 6% to today’s electricity demand and require $450 billion in infrastructure investments by 2040.

Reshuffling the trucking value chain

The transition to EV vehicles will disrupt the entire truck value chain and its players. New players, partnerships, and products are expected. Major roles will be played by large OEMs (OEM) moving directly into cell and pack manufacturing, existing tier-one suppliers entering the field, and pure battery integrator players specializing in packaging.

Some of the major disruptions that may occur include:

A shift toward trucking-as-a-service. This change will affect vehicle provision, financing, aftermarket parts and services, infrastructure, and energy provision.

An increased preference for leasing. Due to the high upfront CAPEX needed to produce EV trucks and the greater technology risks involved in the shift to a new technology, fleet providers will prefer leasing options that also cover charging infrastructure and maintenance.

Greater emphasis on partnerships. Given their smaller scale of operations, individual truck companies are not large enough to participate in every step of the value chain. Instead, they could benefit by forming partnerships that give them access to critical products, such as batteries.